Shipping is an international industry, a business dominated by world geography, yet uniquely unencumbered by national boundaries. Commercial ships are designed not only to sustain the forces of the waters they ply, but also to serve the geographic deficiencies of the continents among which they shuttle. Neither a merchant ship, nor the extensive planning that goes into her, shows respect for purely national interests, for redistributing the earth’s resources is an international concern. Indeed it is not unusual to find a tanker being financed jointly by Greek and American funds, built in a Japanese yard, manned by Italians, owned by a United States corporation, and operating under the Panamanian flag between the Persian Gulf and Northern Europe. National control over such a conglomeration of people, interests, and tasks certainly appears to be unlikely.

Yet underneath this irreverence for national boundaries flow selected and peculiarly national interests. Wartime operational control of merchant tonnage has increasingly come to be a matter of strong national interest. With the rapid advances in technology and the ever-improving living conditions throughout the world, nations are finding themselves forced into alarmingly interdependent roles, pushed by their industrial and social achievements into demand for materials not found at home.

This is the position of the United States at present. Her accelerated technological and industrial power has placed critical emphasis upon imported raw materials to such an extent that since the early 1950s, the availability of transoceanic shipping has come to be a major consideration in both private and government supply planning.

Within this framework of an ever widening international demand for shipping there exists what at first glance appears to be a total anachronism—the Effective United States Control Fleet.

As will be shown later, the EUSC fleet got started when the Administration attempted to retain the most important form of national control over shipping, which, because the operation of shipping under American laws was becoming impossible, was finding refuge abroad under convenient foreign flags. This fleet gave expression to uncomfortable and urgent compromises with reality. It became impossible to operate ships under the national ensign for reasons of modern historical significance, such as the postwar, entrenched position attained by an already highly paid labor force accustomed to war bonuses.

It was impossible to operate ships under the American flag because the costs of ship construction, operations, taxes, and labor (which costs or vested interests were protected by American law), made international competition too stiff for the unsubsidized operator. And international competition is the natural environment of shipping.

Historically, laws relating to prohibition and to neutrality, enacted during America’s pre-World War II isolation, provided the initial impetus for the ship operator to seek a flag of convenience. They also provided the President with the motives to assist the ship operator to survive, and yet to maintain some control, with which he could help potential allies against the Axis before we entered the war, and later to make use of the ships when we entered the war.

In the period after the Second World War, the United States became principally a client shipper, rather than a primary operator of ships to carry other peoples’ goods. American lawmakers have regarded shipping as a national preserve. The country, in framing its laws about merchant shipping, has ignored the real character of the business environment, that is, international competition, on which understanding the owner relies to make his profit.

The conflicting needs gave rise after the war to three elements of privately owned American shipping. The first is a national flag fleet of about 300 subsidized ships, mainly dry cargo liners engaged in this country’s import-export commerce. The second is a national flag fleet of about 600 unsubsidized ships, some in national trade and others in the U. S. export trade. These ships are mainly tankers, or tramp ships and liners who rely on serving in the protected coastal trades or on government contracts for their main income. The third element is the derivatively controlled EUSC, the subject of this essay.

Effective United States control is a concept of emergency control exerted by the government over a substantial number of ships not registered under the U. S. national ensign. Instead, such ships fly the flags of Panama, Liberia, and, less frequently, Honduras. Not all vessels registered in these three countries are subject to U. S. control; only those which have some specific connection with the United States, either because their owners are U. S. citizens, or because their owners have made financially and legally binding commitments. The concept of effective control relies first on the nature of flags of convenience; in this case, the so-called PanHonLib flags, and secondly on the statutory legal base established between the ships and the United States to ensure their availability in wartime.

Although technically responsible to the country whose flag they fly, these ships are also subject to American control during a national crisis. Such control is administered by the Department of Commerce through the Maritime Administration by several means. One of these is the precept that a nation may requisition the property of her citizens during wartime. The EUSC concept depends on the country of registry not opposing legally or practically the principle of American emergency operation. Panama, for instance, acquiesced in the Second World War when tankers, previously transferred to her registry, were used to carry fuel to the allies.

The statutory base for U. S. emergency control is enumerated in the Merchant Marine Act of 1936 which reads in its pertinent parts:

“The owner hereby commits itself to make the vessel available to the United States during any period in which vessels may be requisitioned . . . i.e., whenever the President of the United States of America shall proclaim that the security of the national defense makes it advisable or during any national emergency which may have been declared by the proclamation of the President . . . and expressly agrees that the charter or other contract covering the use of the vessel . . . shall be subject to termination or suspension without notice in the event the United States requests the use of the vessel. . .”

Foreign citizens also operate ships in the effective control fleet. They have made themselves subject to the provisions of this act through the Trade-Out-And-Build Program, established in 1956 by the Maritime Administration. Under this program the transfer of the U. S. flag vessels to Liberian, Panamanian, or Honduran registry was authorized subject to ownership of a majority of stock of the foreign company or subsidiary by U. S. citizens. The terms of the program are phrased in part:

“. . . that the ship, whether owned by the foreign corporate buyer, or any subsequent transferee shall, if requested by the United States or any qualified department or agency thereof be sold or chartered to the United States on the same terms and conditions upon which a vessel owned by a citizen of the United States could be requisitioned for purchase or charter as provided in Section 902, Merchant Marine Act, 1936, as amended. . . .”

Because of the predominance of tankers and bulk carriers in the effective control fleet, the primary contribution of such tonnage, once requisitioned by the U. S. government, would be the importing (and perhaps strategic exporting) of bulk raw materials, fuels, and refined petroleum products. That is, in order to provide the greatest benefit to the United States, the ships of the effective control fleet would carry only the same kinds of cargo they carry now: commodities to support the civilian economy and the industries that produce the munitions of war, while the ships of the U. S. Navy, the Military Sea Transportation Service, and the U. S. flag merchant fleet would supply the direct military support to U. S. and allied forces overseas.

What follows is a detailed analysis of the Effective U. S. Control Fleet and the atmosphere in which it works; the contractual agreements that form its legal base, the pecuniary factors that are its raison d’être, and the state in which it is maintained today.

The EUSC fleet, as it will be referred to hereafter, presently is made up of 412 vessels flying one of the three flags mentioned above. The ownership of some 238 vessels—roughly 60 per cent of the fleet—can be traced to U. S. citizens, who own the ships either directly or through wholly-owned foreign subsidiaries. It is a reasonable assumption that another 10 to 15 per cent of the fleet is indirectly controlled by Americans who own a majority of the foreign company’s stock. The remaining 25 to 30 per cent of the EUSC fleet is owned by Greek, Nationalist Chinese, or PanHonLib interests. These non-U. S. owners have been enticed into the effective control fleet through war risk insurance agreements. These legally and financially binding contracts will be discussed in detail later. The 412 ships are of all sizes, types, and capabilities, and operate throughout the world wherever the demand requires.

What nation would want or even need to bind to itself such a collection of foreign-flag—and often foreign-owned—vessels, especially with the technology and manpower available to the United States today? The answer is not simple. It is suggested by: maritime labor strikes, the structure of international shipping cartels, government subsidy, and the all-important details of chartering agreements. It is again partially revealed in legislative disputes over financial support for American ships, and one sees the result of this many-sided problem blatantly displayed in the docks of practically every major port in the world where U. S. flag shipping is becoming increasingly scarce.

How It Began

The effective control fleet bases its existence upon the old nautical prerogative of an owner registering his ship under a flag other than his own, i.e., under a “flag-of-convenience.” These flags-of-convenience are the maritime ensigns of those countries whose laws allow, indeed, in some cases make it easy for, ships owned by foreign nationals or foreign companies to fly their flags.

While the practice of registering under a foreign flag has only recently come to the forefront in maritime circles, it is not new to the shipping industry. As early as the sixteenth century, English merchants were sailing under the Spanish flag to circumvent the monopolistic regulation regarding trade to the West Indies. By the nineteenth century, English trawler operators were working under the Norwegian ensign in order to evade strict British fishing laws and to take advantage of the low survey and labor costs in Norway.

The first actual use of one of these countries’ flags by a U. S. owner was in 1922 when the United American Lines (owned by W. Averill Harriman) transferred two of its liners, the SS Resolute and SS Reliance, to Panamanian registry as a result of a Department of Justice ruling on the Prohibition Amendment, forbidding the sale or transport of alcoholic beverages aboard American flag vessels, even when they were outside the 3-mile limit. Panama’s liberal registry laws contained no such restrictions: thus, on 5 December 1922, the U. S. colors were lowered and the Panamanian ensign raised as the two ships lay in New York harbor. By 1924, union pressure toward increased operating costs precipitated the transfer of the ships of several major oil company fleets, so that some fifteen vessels were recorded that year by Lloyds Register as flying the Panamanian flag. However, the first usage of such flags for strategic purposes occurred just prior to World War II when the Standard Oil Company of New Jersey, fearing the consequences of Hitler’s power tactics, transferred 25 of its tankers from the registry of the free city of Danzig to Panamanian registry after a worldwide survey of possible countries to which such a transfer might be enacted. When war became imminent, Esso removed the German officers and crews and replaced them with United States citizens to ensure the continued use of the vessels. Because of the Neutrality Act which forbade vessels both owned and manned by Americans to trade with countries involved in war, these ships were kept out of the lucrative European oil trade until the crews were again changed, this time to British. At the request of the U. S. government, 15 more vessels were later transferred to the Panamanian flag to help the allies—all playing an important role in the Battle of Britain.

Liberia first ventured into the profitable tax returns of the merchant marine in 1947 when she admitted the Farrell Lines to her registry, yet she limited the ships so registered to operations along the Liberian coast and required Liberian crews. In 1949, the Stettinius Association of New York secured the passage of more liberal maritime regulations in the African nation and successfully negotiated for tax benefits better than those of Panama for the ship owner—making the Liberian ensign the most attractive flag of convenience in the world.

Earlier, the United Fruit Company of New York, at the request of the government of Honduras, had established a Honduran merchant marine by building a number of refrigerated cargo ships for Honduran registry. Although built in the United States, these reefers never flew the American ensign, having been specifically destined for the Honduran flag. Such an agreement between the United Fruit Company and the Honduran government was only natural, for the banana-oriented nation had long provided the major port facilities, labor, and of course, the bananas themselves exclusively to United Fruit. Perhaps because of strict regulatory laws and high taxes on maritime profits, even now the only use of the Honduran ensign as a flag of convenience is by United Fruit through its majority owned subsidiary, Empressa Hondure[ñ]a de Vapores, for the banana trade.

Large scale use of foreign flags by American owners did not begin until the early 1950s when some large companies found themselves becoming increasingly dependent upon foreign sources for their raw materials. For example, the steel industry began to import iron ore from South America after World War II. At the same time, the reconstruction of Europe and Asia after the war placed a heavy demand on ocean transportation of large, bulk shipments of both fuels and raw materials. Though the United States was at her peak in overall tonnage, built during the war, the vast majority of her ships were dry cargo ships, equipped to handle break bulk freight, but not the large quantities of liquid petroleum, bulk iron ore, coal, bauxite, and other minerals so urgently needed. By the late 1950s U. S. flag operators were being pushed out of the market by the economies of foreign labor both in the construction and operation of ships. Because of stringent U. S. laws, shipowners moved toward the more liberal and profitable laws of flag of convenience countries.

The principal flag of convenience nations are Panama and Liberia. Lebanon, Surinam, and just recently, the Republic of Somalia, also accept foreign owned vessels under their registry for the rather obvious purpose of financial return. (Though United States owners also operate vessels under other flags: those of Belgium, Great Britain, Canada, Denmark, the Netherlands, France, West Germany, Italy, and Norway, those flags are not considered true convenience flags because of their countries’ restrictive attitude toward ownership and state control and their emphasis upon tax earnings from maritime profits.)

Money

The benefits provided by registering under a flag of convenience rather than a traditional maritime flag, such as that of the United States or Great Britain, are threefold; all are based upon the economics of a highly competitive industry. Initially, lower construction costs are the determining factor. By law, if they want to qualify for subsidy, participate in coastal trade, or receive preference on military or AID cargoes, all U. S. registered vessels must be built in the United States and be manned by a crew of which at least three-quarters are U. S. citizens. Conversely the flag of convenience nations carry no such built-in restrictions, thereby allowing the owner to take advantage of the lower construction costs, and until recently, the shorter lead times of overseas yards.

Construction costs vary from country to country and even from yard to yard, yet the price gap between U. S. and foreign yards is considerable. For example an 89,000 dwt bulk carrier built in Japan would cost the owner approximately $8,200,000 whereas the same vessel built to the same specifications in an American yard might run over twice that much or nearly $17,000,000. In addition multiple orders have been pushed out considerably faster in foreign yards through standardization techniques, something just returning to the U. S. shipbuilding industry for the first time in many years. In some cases this has cut the lead time in delivering ships as much as 24 months. Recently however, major foreign yards have been swamped with orders such that many builders are booked well into the 1980s. As of 1 April 1969, Japanese yards had 483 vessels on order or under construction totaling almost 17 million gross tons. The other big winner in ship construction, West Germany, had 227 vessels on order including 136 new dry cargo ships. At the same time U. S. shipyards had only 66 merchant vessels on order or under construction—none of which were in the giant range of foreign-built bulk carriers. These 66 merchant vessels account for three per cent of all merchant ships, or 1.7 per cent of all tonnage, on order throughout the world—an indication of the costs of building in the U. S. Almost every EUSC ship was built abroad.

In fairness to American shipbuilders and in contrast to often voiced statements, American shipbuilders have achieved a high level of productivity while floating some of the safest and most sophisticated ships on the seas today. Using tanker production as a reference, the Center for Maritime Studies (an independent research organization at the Webb Institute of Naval Architecture) reported that U. S. yards consumed 10.9 man-hours per deadweight ton of construction versus 13.3 to 15.9 man-hours in Japanese yards [and] 16.0 in Great Britain. Despite the favorable level of productivity, high wages prevent domestic yards from competing in the international shipbuilding industry. Thus, although Japan’s productivity per workman is only 79 per cent of America’s, its wage rate is one-fourth that paid in the United States. To meet Japanese prices, U. S. yards would have to increase their productivity two and one-half times. Perhaps they could do this, but so might the Japanese.

Operating costs are the second principal reason for foreign registration. U. S. flag tankers and bulk carriers get no federal subsidy, nor are their owners allowed to maintain a tax-free construction reserve from profits, as are U. S. flag liner fleets. When lack of government support is combined with the much higher cost to charter a U. S. flag ship, compared to her foreign flag competitor, the lack of enthusiasm for flying the Stars and Stripes is understandable. For example on 10 September 1960, the SS Venore, a U. S. flag ship owned by the Bethlehem Steel Corp., was chartered to carry a load of grain from the Gulf of Mexico to Bombay at the rate of $17.95 per ton. Simultaneously the SS Silver Hills, a bulk carrier under the flag of Panama, was chartered under identical circumstances for $8.16 per ton. Both vessels measure close to 24,000 dwt and cruise economically at 16.5 knots and both were hired under gross terms—yet the U. S. flag vessel charged two and one quarter times what the Panamanian carrier did; a difference of over $195,000 for the full cargo. These prices result primarily from high price of American labor which can cost the operator four to five times that of foreign crews. Supplies and repairs in U. S. yards contribute to the overall cost differential too.

The tax advantage of foreign registry is the third reason to shift to a foreign flag. In Liberia and Panama initial registration fees are nominal and yearly tonnage taxes run 10 cents and 12 cents per net ton respectively. In both Liberia and Panama earnings derived from shipping are excluded from corporate income tax. Moreover, according to U. S. law, American owners of foreign registered shipping are not subject to U. S. income tax (roughly 50 per cent) until their foreign earnings are repatriated to the United States. The PanHonLib fleet owners therefore have the decided advantage of tax deferment, basically by plowing their earnings back into the fleet, often building a cash reserve for future construction or modernization. Such a tax-free construction fund is not possible to their U. S. flag sister fleets. This is an instrumental bargaining point when bank financing is being sought, and one of the reasons why four-fifths of the EUSC fleet is made up of tankers and bulk carriers.

United States operators are not the only maritime ones to take advantage of flags of convenience. It has been estimated that Greek citizens directly and indirectly control nearly one-half of the ships under Panamanian and Liberian flags. Between them, American and Greek citizens manage more than 80 per cent of the ships under those flags. Most of the remaining 400-odd vessels under those two ensigns can be traced to predominantly Italian and British ownership, but there is some usage of them by citizens of some thirty other free world nations. However other nations customarily deny that their citizens own any of those 400 ships, and such denials are difficult to repudiate in the international maze of agents, operators, and owners. No country other than the United States employs the effective control concept, partially because their national flag shipping is sufficient and, perhaps, because none has the maritime might to back it up.

The increasing frequency of outside registration became evident early in the 1950s. From that unpretentious beginning in 1947, when Liberia allowed the Farrell Lines to register ships in Monrovia, the Liberian ensign has become the most attractive flag of convenience in the world. By 1956 the rush away from the traditional flags of Greece, Great Britain, and the United States and the concurrent drop in U. S. construction orders precipitated what has come to be known as the “trade-out-and-build” program.

The federal subsidy system was proving ineffective, and as a result, the Maritime Administration authorized the sale or transfer of certain U. S. flag vessels to Liberian, Panamanian, and Honduran registry in 1956 under the condition that new ships would be built in American yards to replace the transferred ones. These transfers, involving a varying ratio of new construction to transferred tonnage, are subject to several stringent ownership laws, and require that the transferred ship be, if requested, sold or chartered to the United States under the same provisions as U. S. flag vessels would be. This meant that all vessels so transferred or sold would still be subject to emergency requisition by the government as expressed in Section 902 of the 1936 Merchant Marine Act as previously quoted.

The trade-out-and-build program proved to be only an ineffective stopgap in the ever-increasing tendency for U. S. ship owners to build and register ships outside the U. S. The idea failed to stem the tide partly because the program was no more than a scheme to get new ships built without the federal government paying a construction subsidy, and partly because its provisions called for substantial new construction in return for the trade-out. Hence, the trend to unfettered international arrangements continued with only a momentary pause.

The ships that were transferred under the program were the beginning of today’s EUSC fleet. They were primarily dry cargo ships of the Liberty, C-1, and C-2 classes. Those transferred to PanHonLib registry in the early stages of the program, today make up only seven per cent of the EUSC fleet. They have been forced out by the greater income-returning bulk carriers and tankers built in foreign yards. The Maritime Administration, seeing that it had inadvertently given birth to a more feasible solution to the shipowner’s problems (and perhaps because little new U. S. flag tonnage resulted from the program), initiated the war risk insurance arrangement and began accepting “letters of intent.” Through such bilateral agreements with operators, the Maritime Administration has placed at its command a large, modern, and efficient armada of commercial ships.

It should be noted here that the Department of Defense was not involved in the early stages of the EUSC fleet. The trade-out-and-build program was strictly a product of the Maritime Administration and not a very productive one at that. Circumstances indicate that the Department of Defense first became interested upon establishment of the war risk binders, and quite possibly was responsible at least in part for its coming about. Even the phrase “effective control” is of fairly recent origin, dating from the late 1950s or early 1960s.

Ships

The effective control fleet today consists of 412 oceangoing vessels, ranging in size from the 3,925 dwt coastal Canopus of Panamanian registry up to the giant 327,000 dwt tankers, Universe Ireland and Universe Kuwait of Monrovia. If considered collectively, the EUSC fleet would rank in deadweight tonnage just ahead of the privately owned commercial fleet of the United States. Tankers dominate the fleet, making up two-thirds of the number of ships and 77 per cent of the total tonnage. General dry cargo ships are the smallest segment—comprising only 28 vessels, four of which will have been scrapped by the time this study is published. Most of these 28 ships have been sold or transferred many times since their original switch under the trade-out-and-build program, and it is doubtful if they could stand the demanding sailing schedule likely to develop duringa crisis. (A number of these old timers may be found operating under the Panamanian flag in the tropical waters of the South China Sea and about the Malaysia archipelago where labor is cheap and where a port’s capabilities depend almost wholly upon the size of the work force available.) Bulk carriers have gained considerable importance within the fleet because of their special economic value, and are of a number and capacity exceeded only by the tankers. The rest of the fleet involves a variety of special cargo ships such as refrigerated carriers, chemical and cryogenic ships, and passenger/cargo vessels. A breakdown of numbers is illustrated in the table in the opposite column.

|

|

NO. OF SHIPS |

DWT |

|---|---|---|

|

TOTAL ALL TYPES |

412 |

15,727.2 |

|

1.Dry Cargo |

134 |

3,668.1 |

|

General (23 Libertys, 1-exC3, 2-C2, 2-C1 A/B) |

28 |

299.9 |

|

Bulk Cargo |

95 |

3,316.6 |

|

Reefer Cargo |

9 |

40.4 |

|

Coastal |

2 |

11.2 |

|

2. Passenger Cargo |

8 |

66.7 |

|

3. Tankers |

270 |

11,992.4 |

|

Major Types |

250 |

11,823.7 |

|

18 Knots and Over |

1 |

34.3 |

|

16 to 17.9 Knots |

178 |

8,750.9 |

|

14 to 15.9 Knots |

||

|

T3-S-A1 |

1 |

16.3 |

|

T2-SE-A1 |

10 |

166.2 |

|

Other Designs |

54 |

2,769.4 |

|

Under 14 Knots |

6 |

86.6 |

|

Minor Types (Coastal) |

8 |

30.2 |

|

Special Products |

12 |

138.5 |

__________

Source: Annex to Merchant Ship Register, MSTS P504A dated 16 October 1968 published by Military Sea Transportation Service, Washington, D. C. 20390.

Unless one is thoroughly familiar with the individual ships that make up the EUSC fleet, one would not recognize them by their appearance. They bear no common color scheme or distinctive house markings, and on the high seas they are indistinguishable from the 19,000 other merchant vessels earning their keep in exactly the same way. Part of the fleet is old, nearing the 25-year mark, but it also includes some of the most modern ships anywhere in the world.

|

RANK* |

COUNTRY |

TOTAL NUMBER SHIPS |

RANK |

COUNTRY |

TOTAL DEADWEIGHT TONNAGE** |

|---|---|---|---|---|---|

|

1. |

United States (Total) |

2,101 |

1 |

Liberia |

41,901,000 |

|

2. 1. |

United Kingdom |

1,857 |

2 |

Norway |

30,209,000 |

|

3. 2. |

Japan |

1,664 |

3 |

United Kingdom |

28,119,000 |

|

4. 3. |

Liberia |

1,547 |

4 |

Japan |

26,815,000 |

|

5. 4. |

U.S.S.R. |

1,442 |

5 |

United States |

25,699,000 (15,349,000) |

|

6. 5. |

Norway |

1,352 |

6 |

U.S.S.R. |

10,999,600 |

|

6. |

Greece |

987 |

|

|

|

|

7. |

United States (Private) |

976 |

|

|

|

__________

Source: U. S. Department of Commerce, Maritime Administration Report No. MAR-560-20 dated November 4, 1968.

* The sliding scale shows how the U. S. ranks in total number of ships in two circumstances. She ranks first if all U. S. private-owned, government-owned, and National Defense Reserve Fleet ships are included which together number 2,101 ships as of this counting. She ranks seventh in number of ships if only privately-owned ships are counted.

In a third circumstance the U. S. would change places with Greece if all active U. S. flag ships were counted (1,152 i.e., U. S. privately-owned and non-NDRF government owned ships).

** Similar to the necessary adjustment made to number of ships, it depends on whether one considers all U. S. government and privately-owned flag tonnage, or just privately-owned flag tonnage. The number in parentheses represents the latter.

The criteria by which ships are judged are many. Paramount among these are age, size (or volume), and speed. Most other performance factors may be directly related to one of these characteristics. Because the effective control fleet plays such a large part in the strategic thinking of America, it would be well to compare it with our merchant fleet, using the latter as a yardstick by which to measure the former. In order to place such a comparison in perspective, it should be noted that while the U. S. flag fleet, (both government and privately-owned U. S. flag commercial vessels), is the largest single flag fleet in the world in terms of numbers, that is true only if you include many old government-owned ships in reserve. In reality, in terms of cargo carrying capacity, the Stars and Stripes fly over the fifth largest fleet, well below the fleets of Liberia, Norway, Great Britain, and Japan. It must also be remembered that the inactive government-owned fleet (NDRF) is of marginal value beyond scrap.

The figures at the bottom of the preceding page are offered in support of international fleet rankings.

The relative volume of the two fleets is illustrated in the next column. Here the deadweight ton expresses the total lifting capacity of a vessel in terms of long tons. The U. S. private flag fleet, 976 ships, has 15,349,000 dwt, or about the same as the carrying capacity of the EUSC fleet of 412 ships, yet the size and age of the individual vessels tells a different story. One-half of the EUSC fleet vessels are of a deadweight tonnage greater than 30,000 tons, a strong indicator of the recent trend toward oceangoing giants, while only about 10 per cent of the U. S. flag fleet is greater than 20,000 dwt. In both fleets the large tonnage figures are concentrated in the tankers and bulk carriers. It is the size and speed of just such vessels that are the strength of the EUSC fleet, for EUSC tankers average 16.5 knots while the U. S. privately-owned tankers average 15.0 knots.

Tonnage Breakdown of U. S. Flag and EUSC Fleets

|

|

DWT |

SHIPS |

|---|---|---|

|

Tankers |

6,937,000 |

279 |

|

Bulk Carriers |

999,999 |

52 |

|

Dry Cargo |

7,076,000 |

600 |

|

Other |

337,000 |

45 |

|

TOTAL |

15,349,000 |

976 |

| DWT | SHIPS | |

|---|---|---|

|

Tankers |

11,992,400 |

270 |

|

Bulk Carriers |

3,316,600 |

95 |

|

Dry Cargo |

311,100 |

30 |

|

Other |

107,100 |

17 |

|

TOTAL |

15,727,200 |

412 |

This table also brings out another point that will prove to be critical. In numbers alone the backbone of the U. S. flag fleet is the dry cargo ship. The freighters provide both liner and tramp service to U. S. intercoastal and overseas markets. The EUSC fleet on the other hand has only 28 dry cargo vessels.

The U. S. flag fleet today has had only about 250 new ships added to it since the boost provided by the Second World War.1 The competition which forced U. S. owners to flags of convenience has also forced the building of tankers and bulk carriers in yards outside the United States. The many break-bulk freighters built during the war, now providing berth services to U. S. ports, are still around only because of federal subsidy in one form or another. On their own they could not be operated except at a continuous loss. Through the EUSC concept the U. S. government has indirectly complemented its national flag freighter fleet with the large bulk capacity of the PanHonLib ships.

Age plays a leading role in the assessment of any seagoing vessel. Overall the PanHonLib ships of the EUSC fleet are considerably newer than their American sisters. Only 255 ships (26 per cent) of the U. S. privately-owned are younger than 15 years, while the majority of the EUSC vessels are within the 15-year age bracket. Only 26 per cent of the EUSC fleet has served through 20 years while 67 per cent of the U. S. fleet have steamed the oceans for more than two decades.

The importance of the dry cargo performance is illustrated on the following page. All thirty of the EUSC freighters (including the two coastal freighters listed above) were built prior to 1948 and the bulk of U. S. flag dry cargo ships (C-2, VC-2, and C-3 class ships) were built in the shipping boom of World War II. Yet the construction doldrums of the 1950s have apparently been reversed. Between 1949 and 1959 only 28 commercial break-bulk ships slid down the ways to fly the Stars and Stripes. Since 1960 however, some 85 dry cargo carriers have been built—a trend that is seemingly a result of an increased awareness of our aging maritime fleet.

Speed is often a telling factor in the performance rating of a vessel. EUSC ships average 15.2 knots; the same average speed as America’s privately-owned fleet and a healthy margin over the 12.2 knot average of the U. S. government-owned ships.

Owners

United States incorporated firms control the largest segment of the EUSC vessels through wholly or partially-owned foreign subsidiaries in the PanHonLib countries. Together they operate 238 vessels—over 57 per cent of the entire EUSC fleet. It is an interesting sidelight to note that some 146 of the U. S. corporate owned effective control ships are those of proprietary firms, i.e., integrated oil and other industrial companies. Individual maritime operators have not been the only group to be forced into foreign flag usage. The largest single in-house EUSC fleet is that of Standard Oil Company of New Jersey, which, along with the others of the top ten proprietary fleets, make up 35 per cent of the effective control fleet today.

|

|

Tota Ships |

Under 5 Yrs |

5-9 Yrs |

10-14 Yrs |

15-19 Yrs |

20-24 Yrs |

25 Years1 & Over |

|---|---|---|---|---|---|---|---|

|

TOTAL FLEET |

975 |

82 |

118 |

55 |

67 |

390 |

263 |

|

(percent) |

(100) |

(8) |

(12) |

(6) |

(7) |

(40) |

(27) |

|

1.Dry Cargo |

663 |

69 |

81 |

3 |

24 |

307 |

179 |

|

(percent) |

(100) |

(10) |

(12) |

(*) |

(4) |

(46) |

(27) |

|

General Cargo |

590 |

68 |

78 |

3 |

24 |

264 |

153 |

|

(percent) |

(100) |

(11½) |

(13) |

(½) |

(4) |

(45) |

(26) |

|

Bulk Cargo |

51 |

|

1 |

|

|

26 |

24 |

|

(percent) |

(100) |

|

(2) |

|

|

(51) |

(47) |

|

Reefer Cargo |

15 |

|

|

|

|

15 |

|

|

(percent) |

(100) |

|

|

|

|

(100) |

|

|

Coastal Type |

7 |

1 |

2 |

|

|

2 |

2 |

|

(percent) |

(100) |

(14) |

(28½) |

|

|

(28½) |

(28½) |

|

2. Passenger |

22 |

|

4 |

4 |

6 |

7 |

1 |

|

(percent) |

(100) |

|

(18) |

(18) |

(27) |

(31) |

(5) |

|

3. Tankers |

290 |

13 |

33 |

48 |

37 |

76 |

83 |

|

(percent) |

(100) |

(4) |

(11) |

(17) |

(13) |

(26) |

(26) |

|

Major Types |

251 |

13 |

32 |

44 |

34 |

63 |

65 |

|

(percent) |

(100) |

(5) |

(13) |

(17) |

(13) |

(25) |

(26) |

|

Coastal Types |

25 |

|

|

4 |

2 |

8 |

11 |

|

(percent) |

(100) |

|

|

(16) |

(8) |

(32) |

(44) |

|

Special Products |

14 |

|

1 |

|

1 |

5 |

7 |

|

(percent) |

(100) |

|

(7) |

|

(7) |

(36) |

(50) |

__________

1 3 Dry Cargo, 1 Passenger and 9 Coastal tankers are over 30 years old.

*Less than ½ of 1%.

Source: Merchant Ship Register, MSTS P504.

|

|

Average Age |

0-5 |

6-10 |

Actual Age (Years) |

16-20 |

20+ |

Total |

|---|---|---|---|---|---|---|---|

|

Tankers |

10.9 |

46 |

95 |

61 |

22 |

34 |

258 |

|

Bulk Carriers |

12.6 |

18 |

29 |

14 |

2 |

32 |

95 |

|

Dry Cargo |

22.3 |

— |

— |

— |

— |

30 |

30 |

|

Reefers |

14.0 |

— |

2 |

4 |

2 |

1 |

9 |

|

Other |

13.8 |

6 |

2 |

2 |

— |

10 |

20 |

|

Total |

12.3 |

70 |

128 |

81 |

26 |

107 |

412 |

|

|

|

(17%) |

(31%) |

(20%) |

(6%) |

(26%) |

|

U. S. independents such as the Naess Group (with 12 ships totaling 560,000 dwt in the EUSC fleet) and the D. K. Ludwig enterprises (30 ships of 2,500,000 dwt including the two largest built to date, the 327,000 dwt tankers Universe Ireland and Universe Kuwait) also loom large in the American-owned sector.

Six of the ten companies listed (all but Utah Construction, Bethlehem Steel, Phillips, and United Fruit) are members of the American Committee for Flags of Necessity, an agency in New York representing the interest of American stockholders in vessels registered under the laws of the Republics of Liberia and Panama. With the inclusion of several large independents, the 14-member ACFN has come to be the bulk operator’s equivalent to the former Committee of American Steamship Lines and the present American Institute of Merchant Shipping who represent the subsidized and unsubsidized American fleets.

|

COMPANY |

NR. OF FOREIGN SUBSIDIARIES HANDLING EUSC SHIPS |

SHIPS IN EUSC FLEET |

|---|---|---|

|

Standard Oil Company |

4 |

40 |

|

Texaco, Inc. |

4 |

28 |

|

Standard Oil Company |

2 |

24 |

|

Tidewater Oil Company |

4 |

12 |

|

Gulf Oil Corporation |

2 |

9 |

|

United Fruit Company |

2 |

9 |

|

Aluminum Corp. of America |

1 |

7 |

|

Utah Construction &Mining |

1 |

7 |

|

Bethlehem Steel Corporation |

2 |

6 |

|

Phillips Petroleum Company |

2 |

5 |

|

TOTAL |

24 |

146 |

Because of their close ties with U. S. transoceanic shipping, many of the lesser controlled subsidiaries, i.e., non-wholly owned foreign subsidiaries of U. S. corporations or U. S. citizens, have offices in New York City; yet they may own or charter their vessels from localities as widespread as Monaco or Singapore. The actual agent or operator of many vessels may have no direct dealing whatsoever with the owner. Instead, a maze of paper companies are frequently set up to create a legal labyrinth with the purpose of making pursuit of the actual owner as difficult as possible. Though this situation is not widespread in the EUSC fleet, it is present in certain cases. Frequently the deviousness of owners is not to mask a criminal or untrustworthy operation, but rather to defray or sidestep legally the heavy national taxes levied on maritime profits by countries such as the United States and Great Britain.

Because of their lower costs and thus lower charter rates, EUSC ships could underbid their U. S. flag counterparts should they operate in competition. Yet due to the protective nature of American trade regulations, EUSC vessels and all other foreign flag ships are denied participation in U. S. AID and military assistance cargoes and are prohibited from the cabotage trade along both coasts. But since there is no federal or state restriction as to the nationality of ships importing materials (other than rules prohibiting trade by way of Iron Curtain or Communist Chinese ships), EUSC or foreign flag vessels carry almost all of the bulk imported raw materials to U. S. industry. In addition, U. S. exports (other than military or AID cargoes) are not specifically set aside for U. S. flag vessels, thus much of this trade runs in EUSC bottoms.

The subsidies to U. S. dry cargo ships providing berth services have forced the few freighters still under effective control into tramp schedules or foreign pier schedules, hence the dwindling of the EUSC dry cargo segment. Although U. S. flag bulk carriers receive no direct subsidy payments, they do have the advantage of military and AID contracts. Additionally, by law American flag tankers monopolize the shipment of petroleum and petroleum products from the Gulf to the East Coast. Hence U. S. flag fleets remain in existence principally to carry inter-coastal U. S. trade, to provide containerized or break-bulk berth services, and to support foreign aid and military operations.

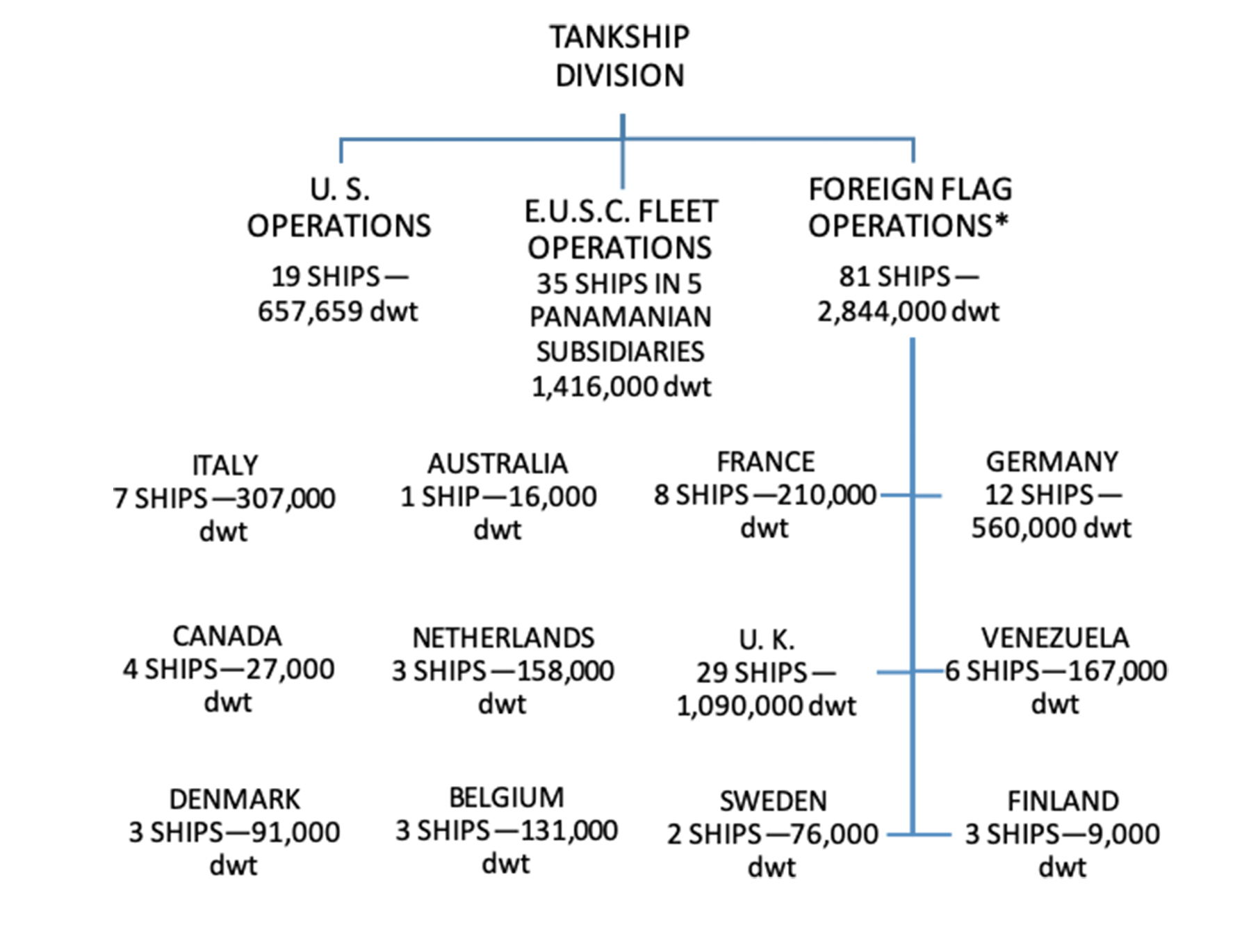

As a result of U. S. trade regulations many large proprietary oil companies maintain three separate fleets; U. S. flag tankers, EUSC vessels, and foreign non-EUSC ships. The leading proprietary company owning ships in the EUSC fleet is a good example of such an operation. As of June 1967, Standard Oil Company of New Jersey carried out operations in 14 countries including the United States. Possibly the world’s largest proprietary fleet, that firm’s foreign tonnage totaled over 4,260,000 dwt divided among 18 subsidiaries. Her international operations chart looks like a Free World United Nations and, grouped according to the three means of control, it might be represented by the accompanying diagram.

*The advantages of non-EUSC foreign flag ships to the U. S. proprietor (such as British, French, and Italian) are that they place the oil company’s ship, and also by extension the oil company itself, in the best possible business relationship to the foreign government. This is the result of these flag fleets serving the country whose flag they fly. This service is rendered by hiring foreign labor, by putting money into the country through taxes and investment. Such ships enjoy the subsidy benefits granted by the registering nation, hence making them that much cheaper to operate for the controlling firm.

Crews

Owing to their varied origins, different areas of operations, and their earnings, effective control ships are manned by many nationalities. European nationals make up the largest single group within the EUSC fleet, particularly the Italians and British. In a study done by the author, more than half the ships observed were run by officers from European NATO countries, while 30 per cent of the ships observed had European crew members. The American Committee for Flags of Necessity reported in 1967 that 50 per cent of their members’ ships were run by Italian licensed and unlicensed personnel, with ships manned by British and Spanish seamen coming next. The rest of the EUSC fleet is operated by an assortment of crews, no one group dominating. These include Hondurans and Panamanians, Indians, Nationalist Chinese, Japanese, Filipinos, Okinawans, Dutch, and Norwegians. Contrary to much public discussion, crew loyalty is not considered a major problem by many of the EUSC owners. Indeed some of the most devoted sailors have been the Italians and Nationalist Chinese, as evidenced by the slow turnover rate among companies employing these people. Certainly the search for cheap labor is one of the principal reasons for running under a flag other than the traditional maritime ensigns, yet there has been no sacrifice of skill and experience. Texaco, Inc., for example, staffs all its Panamanian-flag fleet through offices in Palermo, Sicily, and has consistently been rewarded with conscientious, hard-working, and loyal crew members. Grand Bassra, the wholly-owned Liberian subsidiary of Cities Service Tanker Corporation, mans its vessels with officers and crews from either Formosa or Spain with continuing good results. As C. S. Tietsworth, Vice President of Socony Mobile Oil Company, said before a congressional subcommittee: “We have no reason to doubt the loyalty of either officers or crews serving on our foreign-flag vessels. Socony Mobile Oil Company, Inc., and its predecessor corporations through its affiliates have operated a large number of vessels under foreign flags over a period of more than fifty years, and during this entire period (which includes World War I and World War II) there has not been one incident involving actual or suspected loss of control of a vessel because of a question of loyalty of our maritime personnel.”

One often forgets when considering the crew loyalty problem, the elementary fact that a man goes to sea to earn a living. Crews aboard EUSC vessels receive wages and benefits at least equal to and almost always greater than those received by crews on their own country’s vessels. Flag of convenience ships, and hence EUSC vessels, are non-unionized, a condition closely guarded by operators and constantly under fire from the world’s maritime unions. In the maritime field, as in any other profession, man will follow the best source of income. Disregarding the “extras” that most flag of convenience owners offer their crews to maintain the status quo, it is rather improbable that a man would cut off his paycheck by refusing to sail and thereby effectively blackball himself from future jobs with responsible operators. Indeed the commercial sailor may be compared in many respects to the condottiere; he is paid to perform a service—that of moving goods from one place to another. He will go if he is properly paid, and if he is satisfied with his working conditions. To date no EUSC vessel’s crew has refused to sail to Vietnam when their ship has been scheduled for voyages to the war zone.

Operations

The operations of vessels within the effective control fleet are as diverse as the nationalities that run them. At any given instant the 412 ships are scattered all over the globe, each carrying out the terms of her present contract. In the majority, these ships do not trade between the U. S. and some other place. Indeed, in 20 years many will never enter a U. S. port. The ships of the large proprietary fleets are operated as liners, normally serving one specific trade between two or three ports-of-call; while the independently-owned ships are engaged on a time or voyage charter basis, on the open market. As an illustration of how widespread the fleet actually is, the daily reports from most of the 412 vessels were combined on one specific date and plotted. The results are shown in the accompanying chart. Note the large concentration of vessels along the U. S. East Coast, the northern parts of South America, the Mediterranean, the Persian Gulf, and Indian Ocean. As could be expected from the nature of flag of convenience vessels, this picture looks very much like what might be found if one were to plot all the merchant ships in the world at one moment.

The tankers which carry bulk liquids follow routes directly related to the world distribution of crude oil and its derivatives. Of the 256 EUSC tankers observed in the study, some 90 were directly involved in exporting crude oil from the Persian Gulf to Japan, to Western Europe, and to the United States, while another 50 were participating in the Venezuela to Gulf and East Coast U. S., and in Northern European runs. Those tankers in the trade from South America generally load at either Maracaibo, Venezuela, or the Dutch island of Aruba and head north to U. S. East and Gulf Coast ports, returning via the same route in ballast. Other tankers carry substantial quantities of crude oil and refined petroleum to Great Britain and Northern Europe. There is almost no oil shipped directly from either Venezuelan or Persian Gulf fields into U. S. West Coast ports. Most of the supply for our western areas is produced locally. With the recent discovery of oil along the north Alaskan coastline, it is possible that considerable amounts of crude oil will be carried into West Coast refineries by sea. However, U. S. cabotage laws cover Alaska-West Coast runs, thereby excluding EUSC vessels from the trade. Should the Manhattan project prove successful, the cabotage laws cover this route too.

While the United States imports some 2,260,000 barrels of oil daily, she does have capacity for internal support in the event of a major crisis. American oil-fields contain proved reserves of over 31 billion barrels—the third largest reserve in the world. At the present time we export only a little over one per cent of the total world oil flow in the form of refined products.

The tankers in the EUSC fleet now owned by the large integrated oil companies are chartered as the market demands. During a lull they may carry grain, or even fresh water, but never in conjunction with a petroleum cargo. Because of the expense in preparing a ship for the grain trade after an oil run, and the reverse, those tankers working set liquid routes usually make the return trip in ballast.

Bulk carriers of non-liquid commodities find their source of income in the transporting of iron ore, coal, bauxite, and a variety of other important goods such as sugar and sulphur. EUSC bulk carriers are involved to a great extent in carrying iron ore from Venezuela to Europe and North America, and in hauling to those same continents bauxite from Surinam.

Large quantities of ore are loaded at ports along the Orinoco River in the iron-rich mountains of eastern Venezuela and transported into such Gulf ports as Mobile, New Orleans, and Houston, as well as the East Coast ports of Baltimore, Philadelphia, and New York. Much of the ore received on the West Coast enters at either Portland or San Francisco and originates at Guayaquil, Ecuador and neighboring ports in Peru. Bauxite for aluminum comes primarily from Paramaribo, Surinam, into the same U. S. ports.

Outside of the oil and ore exports from India and Indonesia to Japan and Northern Europe, the other principal trade route of effective control bulk carriers is from South America to Europe. Entering the continent through Antwerp, Bergen, or Rotterdam, iron ore flows at the rate of close to 60 million tons annually to supply the European Common Market’s steel industries. Of this amount, about 10 million tons are imported from South America.

Europe exports very little in the way of bulk metals or minerals except perhaps coal from the British Isles. U. S. bulk exports center around grain and other foodstuffs which are handled by either bulk carriers or tankers depending upon the market conditions. When such shipments are carried as U. S. foreign aid, they come under the 50/50 rule, harnessing 50 per cent of the cargo to U. S. bottoms; the remainder is shipped by contracts agreed to on the market.

The freighters in the effective control fleet are, as previously expressed, few in number and slowing from age. In October 1968 there were 28 non-coastal dry cargo ships comprising that sector of the EUSC fleet and this has since slipped to 24. The total carrying capacity of the 24 ships is 257,000 dwt and they have no effect on the non-liner trade in which they are employed. Unlike the other ship types within the fleet, the break bulk (dry cargo freighters) ships do not follow any particular patterns. In fact when dry cargo ship position reports were plotted, the 23 freighters plotted were found loading or unloading in 23 different ports in 18 different countries. Such ships carry whatever is available; a single load may be so varied as to include lumber, automobiles, bagged rice, barrelled petroleum products, and an endless assortment of consumer and industry goods.

Reefers constitute the smallest individual grouping within the effective control fleet with only nine Freon-circulating cargo carriers under EUSC. The majority of these fly the Honduran flag and wear the colors of United Fruit Company’s “Great White Fleet.” As part of a captive operation, these ships make runs between United Fruit Company’s banana plantations in Honduras, Panama, Costa Rica, and Guatemala, and major ports in North America and Europe. A typical run for the SS Tenadores, a modernized version of the successful Fra Berlanga class, may originate at Puerto Cortes, Honduras, head north through the Yucatan Channel, veer east toward Florida and port hop up the East Coast perhaps stopping at Jacksonville, Baltimore, Philadelphia, and New York. Because of the ripening characteristics of the bananas, she only carries fruit northward. The return trip is made either in ballast or carrying a small amount of dry cargo. United Fruit owns more than 60 reefers (totaling some 350,000 gross tons) under the three flags of convenience, hence such vessels do not compete among themselves; and, because of their captive markets and supply sources, they have relatively little competition from other companies.

Other non-EUSC refrigerated cargo vessels carry not only bananas but also beef, dairy products, and deciduous fruit all over the world; principally to the United States, Northern Europe, and Japan. The beef comes from New Zealand, Australia, and Argentina, the fruit from the Pacific Northwest, Chile, and Argentina. They operate in both liner and tramp modes and today average about 300,000 cubic feet of refrigerated space at speeds of 19-22 knots.

EUSC Agreements

In practice, the effective control principle is carried out by the Maritime Administration through one or a combination of four types of agreements with operators: (1) contracts because of flag transfer (the trade-out-and-build program); (2) U. S. ownership; (3) war risk insurance; and (4) letters of intent. The first two are closely related for, under the trade-out-and-build program, flag transfers required United States citizen ownership of a majority of the stock of the foreign company to which the vessel was transferred. The most reliable and enforceable of the four types of control are those over U. S. citizens’ property and the financial ' considerations of war risk insurance.

In the first case, that of U. S. citizen ownership (exercised either directly or indirectly), the United States has the right and the power to requisition her citizens’ property in the interests of national defense, as we have already seen. Yet, because of the unique status of a ship, the question arises as to whether interference by the country of registry might not overrule the control by ownership. To this end the Republic of Liberia has specifically authorized its Maritime Commissioner to approve arrangements whereby a Liberian flag vessel may be made available for use by another country. This sanction has to date been written into contracts involving only U. S.-owned Liberian flag ships as it was designed solely to oblige the effective control concept. Panama on the other hand has made no such agreement but, given our experience, as well as her dependence upon the U. S. Navy for protection in the event of a global war, she would not be likely to oppose such a move. Moreover, none of the three countries involved depend to any large degree upon the ships in question. The chances that a tanker registered in Monrovia will even once in her 20-year life span enter that African port are small, just as a Panamanian ore carrier quite likely will never put over her lines in Cristobal.

The other prime factor in control over the fleet is war risk insurance. This interim insurance policy is provided by the U. S. government to cover shipowners from the moment their commercial insurance terminates due to the outbreak of a war involving conflict between two of the five major powers. The war risk insurance policies are written to cover a period of 30 days following termination of commercial coverage with extensions dependent on the estimations. Because it involves primarily financial support during the crucial period in which commercial policies are void, war risk insurance has attracted many PanHonLib vessels into the ranks of the Maritime Administration’s EUSC fleet. In return for the financial security provided by the policy, the owner assures the availability of his vessel under the stipulation of the 1936 Merchant Marine Act; i.e., he agrees to make the vessel accessible to the U. S. government in time of national emergency. War risk binders involve nominal fees and are handled through a syndicate of commercial marine underwriters on a vessel-by-vessel basis. As of January 1968, some 227 vessels of the 412 ships then considered under effective control were bound by war risk policies.

Letters of intent are perhaps the least reliable of the four agreements, primarily because they are unilateral in nature. They are written statements from commercial operators and owners to the effect that their ships will be subject to emergency requisitioning should the situation so warrant. Such arrangements are made with the Maritime Administration and represent the good faith of the signers. Most letters of intent in effect today are from major independent operators with considerable financial or family ties to the United States, such as the Naess group. Then, too, some of the marine financing institutions require expressions of availability either in the form of a war risk binder or letter of intent before new construction funds will be released. Such clauses act as insurance for their investments.

An agreement to make his vessel available to the U. S. government has considerable effect upon an owner’s operations. It is an important factor to understand. By so doing, an owner will certainly narrow his market. Many contractors, knowing that any agreement they make is subject to government termination, refuse to charter EUSC vessels, even though such termination could only be taken in a national crisis. However, during a crisis is not the time they want to have to go back to the market for tonnage.

The Control Problem

The legal and financial agreements aside, other practical elements of control play an important role. Certainly a tanker anchored in the Indonesian oil port of Balikpapan is less subject to the physical control of the United States than a vessel moored in the Delaware River. Studies taken on four different dates over the past year show that at any given time there is an average of 16 per cent of the EUSC fleet in or near a United States port. This amounts to roughly 70 vessels. Thus, were the United States to requisition the effective control ships, she would have direct and immediate access to approximately 2,000,000 additional deadweight tons of shipping (on the estimated average of 16 per cent of the total EUSC tonnage). If by no other means, this augmentation could always be acquired through the traditional rule of angary thereby assuring the United States of a substantial immediate increase in cargo carrying capacity. Direct control over the rest of the fleet would be more difficult to attain because of the ships’ distance from the continental United States and the time required to place them on strategic routes.

The requisitioning process can probably best be handled by operating tactfully through the owners and operators (an inherent part of effective control administration) and not by sending U. S. Navy ships to intercept friendly vessels on the high seas. Again it should be noted that the EUSC concept has validity only in a national emergency of such proportion requiring virtually total mobilization.

In the fall and winter of 1967-1968, the author used computers and the analytical technique of mathematical programming to view and test empirically the entire spectrum of factors affecting American control of these 412 ships, considering such necessary statistical information as tonnage, speed, distances, emergency needs, all combined and analyzed. A wartime crisis situation was assumed, with a two-ocean demand for deepwater carriage; then the effective control plan was put into action.

What resulted was a complete rerouting of both U. S. flag and PanHonLib/EUSC flag shipping. Crew loyalty and flag registry were considered, as were the position and capabilities of each ship. Reliability factors were computed, applied, and the fleet reshuffled accordingly. The end product showed that the United States could meet all its domestic economy’s demand for refrigerated goods, could control sufficient tonnage to supply all our liquid bulk needs (crude and refined petroleum), could support 100 per cent of the demand for those goods carried by bulk carriers, and just under 22 per cent of the necessary break-bulk dry cargo ships. In addition, there was enough extra bulk carrying capacity to do some strategic exporting to allied countries.

All this was done on the basis that EUSC ships be used to support only the needs of the domestic economy; and that U. S. Navy, MSTS, and U. S.-flag vessels be fully employed in direct support of the war effort. The study, carried out with the assistance of the U. S. Department of Transportation, and the help of a large number of commercial carriers—both proprietary and independent—put theory into practice and provided the first analytical basis for future effective control policy decisions.

The only true weakness determined by the study was the obvious one, the small capacity of the EUSC break-bulk dry cargo segment. The major flaw of the EUSC fleet is in this area, because just such freighters will be necessary to support the demands of Hawaii, Alaska, and Puerto Rico. The island regions of the United States are particularly vulnerable to the short supply of such vessels, owing to their high percentage of imported goods, both raw and finished. To have a sufficient number of break-bulk ships on these routes would cause U. S. flag ships to be diverted from the military effort, or alternately they would have to be contracted for through spot-charters with foreign owners. In naval war, there is always the element of attrition from commerce raiding, but this is a completely different problem, outside the scope of this paper.

Yet even well adapted theory must find some relation to experience if it is to be of any value in predicting the future. There are only two incidents which pertain to the problem—that of American usage of Panamanian flag tankers to supply the allies in World War II, and the British takeover of her subjects’ vessels flying the Netherlands ensign in World War I. In the former case the government of Panama acquiesced to American take-over while in the latter the Dutch protested vehemently, albeit to no avail.

Though the experience in applying the theory is thin at best, the Vietnam conflict has produced some suggestive results. The United States has never officially put into action the concept of effective control, but the movements of individual vessels with the EUSC fleet have given some indication of what the results might be. During the 12 months ending 31 March 1967, U. S. effective control tankers made 47 voyages to South Vietnamese ports and delivered more than 51,000,000 barrels of petroleum products. In addition, several smaller shallow draft EUSC coastal tankers made 14 voyages to South Vietnam and spent 212 days shuttling between Vietnamese ports and transferring products to and from other vessels, including those of MSTS. It should be pointed out that these voyages were pot in contract with the government but rather for private firms who in turn had won government charters. During 1968, MSTS chartered 21 foreign-flag tankers to meet urgent requirements of the military services, yet none of them were obtained by virtue of EUSC. In fiscal year 1966, for example, 95 per cent of the military cargo carried to Vietnam was shipped under the U. S. flag. However, EUSC and other foreign flag ships did make a small contribution to the sea lift. Throughout the EUSC fleet, whether working directly for the U. S. government, or for private contractors, not a single crew has ever protested against sailing its ship to Vietnam.

Yet, all is not sunny in the effective control picture. As previously shown, owners are not excited about diverting their vessels from profitable commercial contracts to government charters via MSTS unless the ship is between commitments at that moment and the rates are profitable. In the long run, the unfavorable attitude created by having to abort a contract with a shipper carries heavy overtones. MSTS did solicit the owners of EUSC ships in 1968 as to availability of their vessels without actually imposing the 1936 Act (this was done in the manner of a “feeler” rather than a specific request) and were met with hems and haws that boiled down to twelve or thirteen ships—and even some of those were doubtful. This incident shows the great world demand for ocean tonnage, for only three per cent of the fleet was unoccupied at the moment the proposition was made.

The effective control fleet, for all its apparent shortcomings, is perhaps the only truly progressive idea to have been born in the stagnant postwar climate of American shipping. In truth it was initially a makeshift theory, devised to get more ships built in the U. S. without putting them under subsidy. Yet it has more recently evolved into a purposeful and productive force—a force crucially important to both the Department of Defense and commercial shippers. Indeed DOD has claimed the fleet as its own, citing the fleet statistics constantly as the one feasible solution to a dearth of international shipping in the event of an emergency. Both the offices of Emergency Transportation and Emergency Planning, which work directly for the President, have alluded to the EUSC fleet’s lifting capacity to such an extent as to have surrounded the 412 ships with an aura of reliability.

These U. S. government agencies consider the fleet in the only perspective that is practical, as the shipping required to carry those commodities needed to support our civilian economy. The effective control fleet is made up of commercial ships carrying commercial cargo with civilian crews serving a civilian market. Simply diverting some of them from their regular tasks to carrying more crucial commercial commodities such as minerals, oil, and grain certainly creates very little doubt in their reliability. Indeed, in war, many would very likely continue “steaming as before.” Together, U. S. Navy, MSTS, and U. S. flag vessels are fully capable of supporting directly any war effort likely to occur, according to testimony recently given before Congress by both the Assistant Secretary of Defense and the Secretary of Commerce. The effective control fleet makes supporting the needs of a civilian economy, even one that is mobilized, easier to solve, which is just what the effective control principle is all about.

The EUSC may not be a panacea for the problems of U. S. flag shipping but it does present a workable and entirely realistic intermediate solution. Until such time that the myriad American shipping interests can be jelled into a single constructive national program, the single star and stripes of Liberia and the starred and quartered ensign of Panama will continue to play a principal role in United States overseas shipping.

[signed] Sidney W. Emery, Jr.

1. In the twenty-year period following the Second World War (1945-1965) only 127 tankers, 129 freighters, and 10 bulk carriers were built in the United States for American registry. In contrast, during the few years of World War II, U. S. yards built thousands of ships.